In the rapidly intensifying climate crisis era, corporations increasingly need to champion the cause of sustainability and guide the global economy toward comprehensive decarbonization.

Recognizing the urgency, the European Commission has taken a decisive path by actively propelling regulatory enhancements to bolster this transition. As we saw in our recent analysis, the EU’s adoption of the European Sustainability Reporting Standards (ESRS) to improve the Corporate Sustainability Reporting Directive (CSRD) is a critical milestone in that direction.

Understanding the nuances of these regulations is non-negotiable. Specifically, organizations must fully understand the complexities of classifying, reporting, and calculating carbon emissions as delineated by the Greenhouse Gas (GHG) Protocol, which divides emissions into three distinct scopes.

This article delves deep into these categorizations, highlighting their pivotal role as banks and companies gear up to report within the CSRD and ESRS frameworks.

What is the Greenhouse Gas (GHG) Protocol?

The GHG Protocol, initiated in 1998, is a global standard for carbon accounting and reporting. Created by the combined efforts of businesses, NGOs, and governments, it was spearheaded by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD).

Its main goal is straightforward: to set universal standards for measuring and reporting greenhouse gas emissions. With its guidelines, the GHG Protocol ensures that organizations everywhere can consistently and clearly report their emissions.

From direct to indirect: understanding the layers of scope 1, 2, and 3 emissions

Source: Greenhouse Gas Protocol – Technical Guidance for Calculating Scope 3 Emissions (Version 1)

Scope 1: direct emissions

Scope 1 emissions originate directly from sources owned or controlled by an organization. Key examples include:

Facility Operations: Greenhouse gases released during the combustion of fossil fuels in boilers or furnaces within company premises.

Company Fleet: Emissions stemming from company-owned vehicles, be it delivery trucks, staff cars, or heavy machinery.

Industrial Processes: Certain industries, like cement production, emit greenhouse gases inherently during their operations.

What sets Scope 1 apart is the company’s hands-on control over these emissions. They offer a direct lens into a company’s environmental impact and set the baseline for its carbon reduction strategy.

Addressing these emissions might mean upgrading to energy-efficient boilers, transitioning to electric vehicles, or adopting innovative production methods – all of which can significantly mitigate a company’s carbon footprint.

Scope 2: indirect emissions

Scope 2 emissions encompass those greenhouse gases resulting from generating the electricity, heat, or steam that an organization purchases and consumes. Unlike Scope 1, which deals with direct emissions from owned or controlled sources, Scope 2 focuses on the emissions produced to generate the energy bought by the company.

So, for example, while a bank’s headquarters might not directly emit greenhouse gases, the electricity it uses to power its operations – from ATMs to data centers – does contribute to emissions at the power plant where that electricity is generated.

Similarly, a financial institution may reside in a skyscraper that uses centralized heating or cooling. The energy consumed for this purpose can produce emissions externally at the source of generation.

In this context, the GHG Protocol’s Scope 2 Guidance standardizes how corporations measure these emissions, providing clearer methodologies to measure emissions from their energy purchases, and it stands as a significant enhancement to the Corporate Accounting and Reporting Standard.

The goal is to ensure financial institutions and other corporations can accurately assess their indirect carbon footprint. By understanding and measuring their impact, businesses in the financial sector can make more informed decisions about sourcing energy or investing in carbon-neutral alternatives.

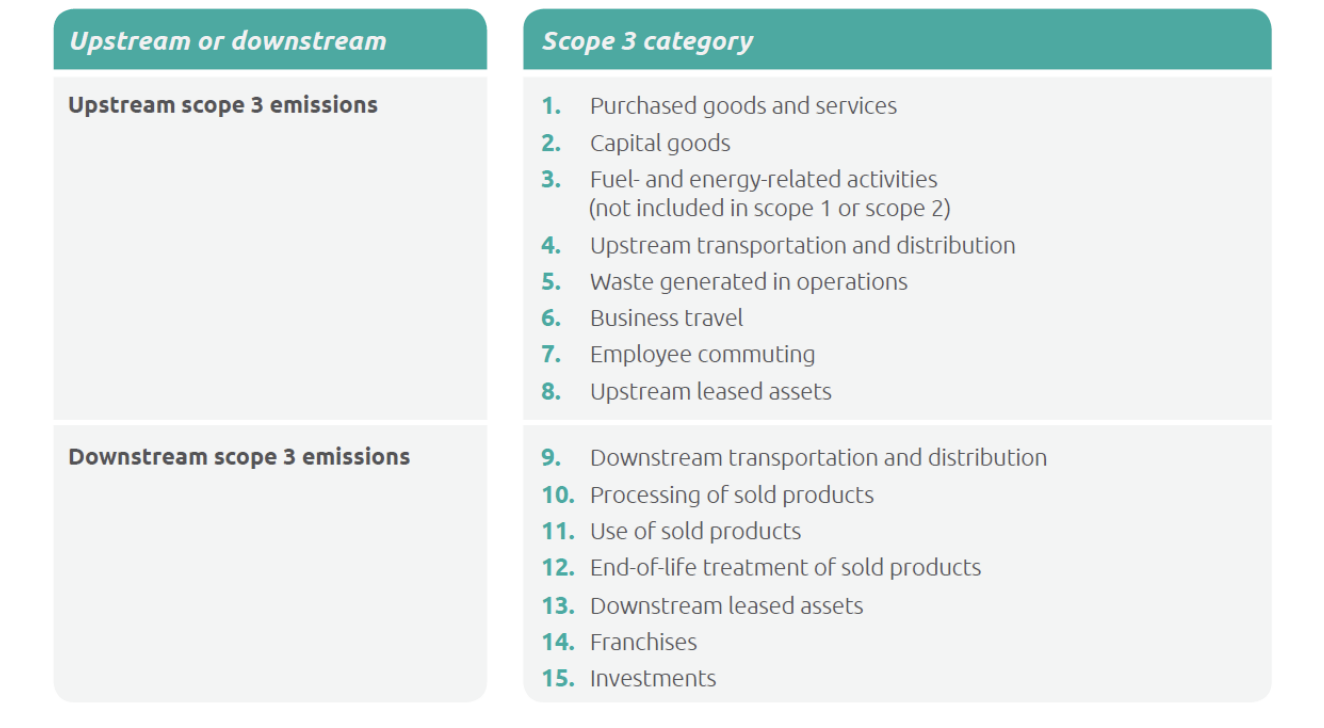

Scope 3: indirect emissions beyond energy purchases

Scope 3 encompasses the most comprehensive category of indirect emissions. So, if Scope 1 and 2 focus on emissions from owned sources and energy purchases, while Scope 3 captures all other indirect emissions occurring throughout a company’s value chain.

The Scope 3 Standard categorizes emissions into upstream and downstream activities, offering a comprehensive view of a company’s carbon footprint. The differentiation is fundamentally tied to the company’s financial transactions.

Upstream emissions encapsulate the indirect GHG emissions arising from goods and services that a company purchases or acquires. On the flip side, downstream emissions account for those indirect GHG emissions linked to the goods and services a company sells. This structured approach ensures that every facet of a company’s operational impact is considered in its GHG assessment. The complete list of categories can be found in the table below.

Source: Greenhouse Gas Protocol – Scope 3 Frequently Asked Questions.

As it’s probably evident at this point, navigating the complexities of Scope 3 emissions calculation is undeniably challenging for companies.

However, it’s vital to recognize that the path to net zero requires consideration of these emissions, particularly as the new ESRS and the CSRD further shape the corporate reporting realm. That’s true, especially if we consider that even if these emissions might fall outside the direct control of the reporting company, they can constitute a large segment of its total carbon footprint.

Calculating carbon emission with AI

At Dydon AI we are eager to find solutions with our artificial intelligence models to overcome the dilemma of lack of data by introducing appropriate models for calculating carbon emissions and other technical criteria that are needed within the evaluation of the economic activities of the EU Taxonomy.

With that need in mind, at Dydon AI, we’ve developed the Taxo Tool as a tangible solution tailored around the EU Taxonomy to provide businesses with a reporting solution to stay compliant and accelerate the transition to carbon neutrality. And more to come for the Scope 1, 2, 3 carbon emissions calculation, stay connected.